Here’s a story you’ve probably heard before: Chioma, a 32-year-old software developer in Lagos, received what seemed like a life-changing email—a job offer from a tech company in Toronto, Canada. The salary was impressive: CAD $85,000 annually. But then reality hit. Between visa application fees, medical examinations, police certificates, biometrics, proof of funds, flight tickets, and initial accommodation costs, she needed approximately ₦8.5 million (roughly $5,500 USD) upfront. Her savings? Only ₦2.1 million.

This is the relocation paradox: the opportunity of a lifetime blocked by a financial wall that feels insurmountable. And Chioma isn’t alone. According to recent migration data, over 15,000 Nigerians successfully relocated to Canada, the UK, and the USA for work in 2024 alone—and a significant portion of them bridged this financial gap through structured loans and strategic financing.

But here’s what most relocation advisors won’t tell you upfront: borrowing money to relocate is only smart when you’ve already secured a verified pathway. Without confirmed work permit eligibility, employer sponsorship, and a realistic understanding of the total cost, that loan could turn from a bridge to your dreams into a debt trap that haunts you for years.

1.2 The Current Landscape of Migration Finance

The landscape of migration financing has evolved dramatically. Gone are the days when relocating abroad was exclusively for the wealthy or those with family abroad. Today’s Nigerian professionals are increasingly turning to regulated financial institutions, employer-backed relocation packages, and structured personal loans to fund their international career moves.

However, this rise in accessibility has also created a dangerous proliferation of unregistered lenders, fake immigration agents, and “pay after arrival” schemes that prey on desperate job seekers. The key difference between successful relocation and financial disaster? Strategic planning, proper verification, and choosing legitimate financing options.

This comprehensive guide will walk you through every critical step—from verifying your visa pathway to calculating real costs, choosing safe loan options, understanding interest rates, assessing risks, and creating backup plans. Whether you’re eyeing a skilled worker visa for Canada, employer sponsorship in the UK, or an H-1B pathway to the USA, this article will help you make informed financial decisions.

2. The Golden Rule: Verify Your Job and Visa Pathway First

Critical Warning: Never Borrow Before Verification

Before you approach any lender, bank, or even family member for relocation funds, you MUST have verified answers to these questions. Taking out a loan based on promises, unconfirmed job offers, or vague assurances is the fastest route to financial ruin.

2.1 Confirming Job Offers and Employer Legitimacy

Your first step isn’t finding a loan—it’s confirming that your job offer is legitimate and that your employer has the legal authority to sponsor you. Here’s how to verify:

- Request Official Documentation: A genuine job offer should come on company letterhead with specific details including job title, salary, start date, and confirmation of sponsorship.

- Verify Employer Licensing in Canada: For Canada, your employer must obtain a Labour Market Impact Assessment (LMIA) or be LMIA-exempt. You can verify this through Immigration, Refugees and Citizenship Canada (IRCC). The LMIA confirms that no Canadian worker is available for the position and that hiring a foreign worker won’t negatively impact the Canadian labor market.

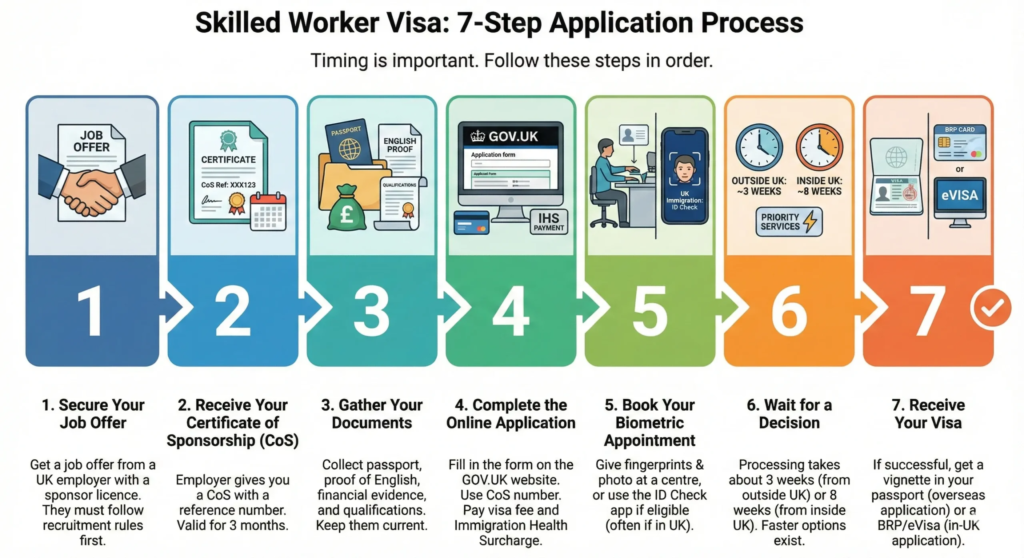

- Check UK Sponsor License: For the UK, employers must hold a valid Sponsor License from the Home Office. You can verify this on the UK government’s official register of licensed sponsors. Without this, they cannot issue you a Certificate of Sponsorship (CoS), which is mandatory for a skilled worker visa.

- Confirm US Employer Petition: For the USA, your employer must file a petition (typically Form I-129 for H-1B visas) with U.S. Citizenship and Immigration Services (USCIS). Always request the receipt notice as proof.

- Research the Company: Use LinkedIn, Glassdoor, and official business registries to confirm the company exists, has actual employees, and operates in your field. Be extremely wary of companies with no online presence or those requesting payment for job offers.

2.2 Understanding Visa Pathways and Eligibility

Each destination country has specific work permit eligibility requirements. Understanding these before seeking financing is crucial:

Canada Skilled Worker Requirements

Canada primarily uses the Express Entry system for skilled workers. Your eligibility depends on factors including age, education, work experience, language proficiency (IELTS or CELPIP for English; TEF for French), and adaptability. You’ll need to score sufficient Comprehensive Ranking System (CRS) points. Alternatively, a valid job offer with LMIA can significantly boost your chances or qualify you under employer-specific streams.

UK Skilled Worker Visa Criteria

The UK skilled worker visa requires a job offer from a licensed sponsor, a Certificate of Sponsorship, meeting the minimum salary threshold (generally £38,700 annually or the “going rate” for your occupation, whichever is higher), and English language proficiency at level B1 (CEFR). Your job must also be on the eligible occupation list.

USA Work Visa Pathways

The USA offers several work visa categories, with H-1B being most common for skilled workers. Requirements include a job offer in a specialty occupation, at least a bachelor’s degree (or equivalent), and employer sponsorship. Note that H-1B visas are subject to annual caps and lottery systems, adding uncertainty to the timeline.

Work with a Licensed Immigration Consultant: Before committing to any loan, invest in a consultation with a Regulated Canadian Immigration Consultant (RCIC) for Canada, an Immigration Adviser regulated by the Office of the Immigration Services Commissioner (OISC) for the UK, or a licensed immigration attorney for the USA. This upfront cost (typically ₦150,000 – ₦500,000) can save you millions in wasted loan repayments for ineligible applications.

Read Also: LMIA Approved $37/h Manufacturing Jobs in Canada – Apply from Abroad

3. The Real Price Tag: Understanding the Total Cost of Relocation

One of the biggest mistakes aspiring migrants make is underestimating the true cost of relocation. Here’s a realistic breakdown of what you’ll actually need:

3.1 Breakdown of Mandatory Visa and Travel Fees

These are non-negotiable expenses you must budget for:

| Expense Category | Canada (CAD) | UK (GBP) | USA (USD) |

|---|---|---|---|

| Visa Application Fee | $155 – $255 | £719 – £1,500 | $190 – $460 |

| Biometrics | $85 | Included | $85 |

| Medical Examination | ₦120,000 – ₦180,000 | ₦150,000 – ₦200,000 | ₦100,000 – ₦150,000 |

| Police Certificate | ₦15,000 – ₦30,000 | ₦15,000 – ₦30,000 | ₦15,000 – ₦30,000 |

| Language Test (IELTS) | ₦95,000 | ₦95,000 | ₦95,000 |

| Flight Ticket (One-way) | ₦800,000 – ₦1,500,000 | ₦600,000 – ₦1,200,000 | ₦900,000 – ₦1,800,000 |

| Immigration Consultant Fees | ₦500,000 – ₦2,000,000 | ₦400,000 – ₦1,500,000 | ₦600,000 – ₦3,000,000 |

Note: Exchange rates fluctuate. Always check current rates when budgeting. Figures converted at approximate rates as of early 2025.

3.2 Proof of Funds and Initial Settlement Costs

Beyond application fees, immigration authorities want proof that you can support yourself upon arrival. These requirements vary:

- Canada Proof of Funds: If you’re applying through Express Entry without a valid job offer, you must show approximately CAD $13,310 for a single applicant (more for families). Even with a job offer, having settlement funds demonstrates financial stability.

- UK Maintenance Funds: You may need to show £1,270 in your bank account for at least 28 consecutive days before applying, unless your sponsor certifies they’ll cover initial costs.

- USA Financial Support: While not always mandatory for H-1B visas, showing financial stability strengthens your application and helps with initial settlement.

Initial Settlement Costs Often Overlooked:

- First month’s rent plus security deposit: ₦600,000 – ₦2,500,000

- Basic furniture and household items: ₦300,000 – ₦800,000

- Winter clothing (Canada/UK): ₦150,000 – ₦400,000

- Phone plan and SIM card: ₦20,000 – ₦50,000

- Transportation card/public transit: ₦30,000 – ₦80,000

- Groceries for first 2-4 weeks: ₦80,000 – ₦200,000

- Emergency fund for unexpected expenses: ₦300,000 – ₦600,000

Total Realistic Budget: For most Nigerians relocating to Canada, the UK, or USA through work permits, expect to need between ₦5,000,000 – ₦12,000,000 ($3,200 – $7,700 USD) depending on your specific pathway, family size, and destination.

This is why proper budgeting—not blind borrowing—is essential. Understanding your true costs helps you borrow only what you need and can realistically repay.

4. Safe Financing Options: Types of Loans You Can Trust

Now that you’ve verified your pathway and calculated your true costs, let’s explore legitimate financing options. The key word here is legitimate—regulated, transparent, and legally enforceable.

4.1 Regulated Personal and Education Loans

Personal Bank Loans

How They Work: Traditional banks like GTBank, Access Bank, First Bank, UBA, and Zenith Bank offer personal loans with fixed terms. You’ll need to demonstrate income, provide collateral (sometimes), and undergo credit checks.

Typical Terms:

- Loan amounts: ₦500,000 – ₦10,000,000

- Interest rates: 18% – 30% annually (varies by bank and creditworthiness)

- Repayment period: 12 – 60 months

- Processing time: 1 – 3 weeks

Advantages: Regulated by the Central Bank of Nigeria, transparent terms, legal recourse if issues arise, credit building opportunity.

Disadvantages: May require collateral, strict eligibility criteria, lengthy application process.

Education Loans (For Study-to-Work Pathways)

If you’re pursuing a student visa route (which can lead to post-graduation work permits), education loans offer advantages:

- Longer Repayment Windows: Often 5-10 years with grace periods

- Lower Interest Rates: Sometimes subsidized or preferential rates (15% – 25%)

- Moratorium Periods: Repayment may not start until after graduation

- Providers: FSDH, Sterling Bank Education Loans, specialized platforms like Prodigy Finance or MPOWER Financing (for international students)

4.2 Employer-Backed Support and Ethical Borrowing

Employer-Sponsored Relocation Packages

The safest financing option is when your employer covers relocation costs upfront, then deducts repayment from your salary over an agreed period.

How It Works:

- Employer pays visa fees, flights, and sometimes initial accommodation

- You sign a contract agreeing to work for a specified period (typically 1-3 years)

- Monthly deductions from salary (usually 10%-20%) until costs are recovered

- If you leave early, you may owe the balance

Why It’s Safer: No upfront debt, interest-free or low-interest, tied to verified employment, legally structured.

What to Absolutely Avoid

- Unregistered Lenders: Individuals or groups offering loans outside the banking system with unclear terms

- “Pay After Arrival” Agents: Migration agents who promise to process your visa for payment only after you land abroad—often scams or involving fraudulent applications

- Social Media Lenders: Loan offers through WhatsApp, Facebook, or Instagram groups with no verifiable credentials

- Loan Sharks: Informal lenders charging exorbitant interest (50%-100%+ annually) with aggressive collection practices

- Advance Fee Fraud: Anyone asking for payment upfront before providing services or securing your visa

5. The Financial Fine Print: Interest Rates and Repayment Plans

Understanding the true cost of borrowing is critical. A ₦5 million loan might sound manageable until you realize you’ll repay ₦8 million over three years. Here’s how to analyze loan terms properly:

5.1 Analyzing Interest Rates and Monthly Installments

Questions You Must Ask Every Lender:

- What is the exact annual interest rate? Ensure it’s stated as Annual Percentage Rate (APR), not monthly rates that seem smaller but compound to much higher actual costs.

- Is the interest rate fixed or variable? Fixed rates stay the same throughout the loan period; variable rates can increase, raising your payments unexpectedly.

- What is the total repayment amount? Don’t just focus on monthly installments—ask for the total you’ll pay over the loan’s life (principal + all interest).

- What are the monthly installments exactly? Get this in writing. Ensure it fits your budget both before and after relocation.

- When does repayment start? Immediately, or is there a grace period? Some lenders offer 1-3 month moratoriums.

- Are there early repayment penalties? If you want to pay off the loan early (perhaps with your first few salaries abroad), will you be charged extra fees?

- What are the late payment penalties? Understand the consequences if you miss a payment—additional interest, penalty fees, credit score damage, or legal action.

Example Calculation:

Let’s say you borrow ₦6,000,000 at 24% annual interest for 36 months:

- Monthly payment: approximately ₦237,000

- Total repayment: approximately ₦8,532,000

- Total interest paid: ₦2,532,000 (42% of the original amount!)

This is why interest rates matter enormously. Even a 5% difference in rates can mean hundreds of thousands of naira in additional costs.

5.2 Creating a Realistic Repayment Strategy

Before signing any loan agreement, create a detailed repayment strategy based on your expected income abroad:

Income vs. Repayment Analysis

Step 1: Calculate Your Expected Net Income Abroad

If your job offer is CAD $70,000 annually in Toronto:

- Gross monthly: CAD $5,833

- After taxes (approximately 25%): CAD $4,375

- In Naira (at ₦1,100/CAD): approximately ₦4,812,500

Step 2: Deduct Essential Living Expenses

- Rent (1-bedroom in Toronto): ₦1,100,000 – ₦1,800,000

- Utilities: ₦80,000 – ₦150,000

- Groceries: ₦250,000 – ₦400,000

- Transportation: ₦100,000 – ₦200,000

- Phone/Internet: ₦50,000 – ₦80,000

- Health insurance (if not covered): ₦50,000 – ₦100,000

- Miscellaneous: ₦100,000 – ₦200,000

Total Essential Expenses: ₦1,730,000 – ₦2,930,000

Step 3: Calculate Maximum Sustainable Loan Payment

Remaining after essentials: ₦1,882,500 – ₦3,082,500

Safe loan payment (maximum 30% of remaining): ₦564,750 – ₦924,750

This analysis shows that monthly loan payments of ₦237,000 (from our earlier example) would be manageable, leaving you room for savings, remittances, and unexpected expenses. However, a loan requiring ₦500,000+ monthly could strain your finances dangerously.

Pro Tip: Always build in a buffer. Currency exchange rates fluctuate, cost of living can be higher than expected, and you may face unexpected expenses. Don’t commit to loan payments that consume more than 20-25% of your expected income abroad.

6. Navigating Risks and Ensuring Legal Protection

Even with verified pathways and careful planning, relocation carries inherent risks. Smart migrants acknowledge these risks and prepare for them.

6.1 Risk Assessment and Avoiding Scams

Primary Risks You Must Consider:

- Visa Denial: Even strong applications can be refused. Processing times vary (3-12 months typically), and during this time, circumstances can change. What’s your plan if your visa is denied after taking the loan?

- Job Offer Withdrawal: Occasionally, employers rescind offers due to business changes, economic conditions, or their own immigration compliance issues. This can happen even after you’ve invested thousands.

- Processing Delays: Immigration processes rarely go exactly as planned. Delays can mean additional accommodation costs, lost opportunities, or expired documents requiring renewal fees.

- Currency Exchange Fluctuations: If you’re earning in CAD, GBP, or USD but repaying a Naira loan, exchange rate movements can significantly affect your real repayment burden.

- Higher Cost of Living Than Expected: Online estimates may not reflect reality. Accommodation might be more expensive, or you might live farther from work than planned, increasing transportation costs.

- Unemployment Upon Arrival: If your employer sponsorship falls through or you lose your job shortly after arrival, you may struggle to meet loan obligations while job hunting in a new country.

Red Flags of Relocation Scams

- Guaranteed visa approval regardless of your profile

- Requests for payment before services are rendered

- No physical office address or verified company registration

- Pressure to act immediately without time to review documents

- Job offers without interviews or skills verification

- Unusually high salaries for entry-level positions

- Agents claiming “special connections” with immigration authorities

- Requests to lie on applications or submit false documents

- Inability to provide client references or success stories

- Communication only through social media or WhatsApp (no official email)

6.2 Legal Safety and Backup Planning

Essential Legal Protections:

- Written Contracts for Everything: Whether it’s a loan agreement, immigration consultant contract, or employer relocation package, insist on detailed written agreements. Verbal promises mean nothing if things go wrong.

- Verify Immigration Consultant Credentials: Ensure your consultant is properly registered (RCIC for Canada, OISC for UK, licensed attorney for USA). Check regulatory body websites for verification.

- Confirm Employer Registration: Independently verify that your employer exists, is registered with appropriate business authorities, and holds necessary sponsor licenses.

- Avoid Fraudulent Schemes: Never participate in fake marriage arrangements, false employer sponsorships, or document fraud. These can result in permanent immigration bans, criminal charges, and wasted money.

- Review Contracts with Legal Counsel: Before signing any significant loan agreement or relocation contract, have a lawyer review it. This cost (₦50,000 – ₦200,000) is minimal compared to potential losses from predatory terms.

Creating Your Backup Plan:

Essential Questions for Your Plan B

- What if my visa is refused? Can I still repay the loan from my current Nigerian income? How long would it take? Would I need to sell assets?

- Is there insurance or a refund policy? Some immigration consultants offer partial refunds if your application is refused due to their error (not applicant ineligibility). Loan insurance products exist that cover payments if you become unemployed.

- Do I have emergency savings? Beyond the loan, maintain an emergency fund of at least 3-6 months of expenses. This buffer protects you from unexpected costs or income disruptions.

- What are my alternative income streams? Can you freelance, consult, or generate side income to help with loan repayments if needed?

- Have I discussed this with family? Transparent communication with family members about your plans, risks, and potential need for support creates a safety net.

Remember: responsible borrowing means preparing for the worst while working toward the best. If you cannot comfortably handle loan repayments should your relocation plans fail, you’re borrowing too much or moving too soon.

7. Conclusion

7.1 Smart Planning for a Successful Move

Relocating to Canada, the UK, or the USA as a Nigerian professional is absolutely achievable—thousands do it successfully every year. The difference between those who thrive and those who struggle often comes down to financial preparation and strategic planning.

Let’s recap the essential steps for using structured loans responsibly:

- Verify First, Borrow Later: Never take a loan before confirming your work permit eligibility, employer sponsorship legitimacy, and visa pathway viability. Consult with licensed immigration professionals.

- Calculate True Costs: Budget for all expenses—visa fees, medical exams, flights, proof of funds, and initial settlement costs. Avoid underestimating; better to borrow slightly more from legitimate sources than scramble for emergency funds from risky lenders.

- Choose Safe Financing: Use regulated banks, education loan programs, or employer-backed relocation packages. Avoid unregistered lenders, social media loan offers, and “pay after arrival” schemes.

- Understand the Fine Print: Know your interest rate (APR), total repayment amount, monthly installments, payment start date, and any penalties. Calculate whether you can afford payments based on realistic income abroad.

- Assess and Mitigate Risks: Acknowledge that visas can be denied, jobs can fall through, and costs can exceed estimates. Create backup plans and maintain emergency savings.

- Protect Yourself Legally: Use written contracts, verify all credentials, and work only with licensed professionals. Never participate in fraudulent schemes.

- Build Financial Discipline: Your relocation journey is a marathon, not a sprint. Prioritize saving where possible, reduce unnecessary debt, and approach borrowing with caution and respect for long-term consequences.

The opportunity to build a career in Canada, the UK, or the USA can be life-changing—better salaries, professional development, quality of life improvements, and pathways to permanent residence and citizenship. But these benefits only materialize when your relocation is built on a foundation of verified pathways, realistic budgeting, and responsible financing.

Final Call to Action

Your next steps should be:

- Research work permit eligibility requirements for your target country and occupation

- Connect with licensed immigration consultants for professional assessment

- Calculate your realistic relocation budget using the guidelines in this article

- Approach regulated financial institutions for loan options if needed

- Review all contracts with legal counsel before signing

- Create a comprehensive timeline and backup plan

Remember: Speed is not success. Careful planning is. Take the time to do this right, and your relocation dreams can become sustainable reality rather than financial nightmare.

The path from Nigeria to international career success is well-worn by those who came before you. Learn from their experiences, avoid their mistakes, and build your future on solid financial ground. Your dream career abroad awaits—but only when you approach it with eyes wide open and finances properly secured.

Safe travels, and may your relocation journey be both successful and financially sustainable.

Disclaimer

This article is provided for informational and educational purposes only and does not constitute financial, legal, or immigration advice. Immigration laws, visa requirements, and loan terms vary by individual circumstances and change frequently. Always consult with licensed immigration professionals, regulated financial advisors, and legal counsel before making relocation or borrowing decisions. The author and publisher assume no liability for actions taken based on information in this article.